Wallet Transaction Enrichment: Why Apple Pay and Google Pay Data Is Harder to Enrich

Digital wallets have fundamentally changed how payments move through the financial system. Apple Pay, Google Pay, Samsung Pay, and other wallet platforms now process billions of transactions annually. Digital wallets collectively accounted for over $13.9 trillion in global transaction value in 2023, according to Worldpay's Global Payments Report, offering consumers faster checkout, stronger security, and better privacy. For users, the experience is seamless: tap your phone and go.

For developers building financial products, that seamlessness creates a significant technical challenge. The same privacy and abstraction features that make wallets convenient for consumers also make wallet transaction enrichment considerably harder than enriching traditional card transactions. The merchant data that enrichment systems rely on is deliberately reduced, abstracted, or reformatted by the wallet layer before it ever reaches a bank feed.

This is not a temporary problem that will be fixed with better data standards. It is a structural consequence of how wallets are designed. Any fintech product that displays transaction data to users, and any transaction enrichment API that processes that data, must understand why wallet transactions are different and how to handle them effectively.

How Wallet Transactions Differ from Card Transactions

A traditional card transaction represents a relatively direct relationship between a cardholder, a merchant, and an acquiring bank. The transaction descriptor flows from the merchant's payment terminal through the acquirer and card network to the issuing bank, carrying the merchant's configured name, location, and category code along the way. While this data is far from perfect, it provides a workable starting point for enrichment.

Digital wallet transactions introduce an additional layer between the consumer and the merchant. The wallet acts as a mediator: it tokenizes the consumer's payment credentials, may aggregate multiple payment sources (credit cards, debit cards, bank accounts), and often standardizes or reformats how transactions appear when they reach bank feeds and data aggregators. Resolving the underlying business behind that wallet label is a merchant identification problem — the same problem we cover end-to-end in our guide on how to enrich raw transaction data with clean merchant names.

The practical differences are significant. Traditional card transactions usually include an explicit, merchant-defined descriptor. Wallet transactions often show a generic or wallet-standardized label. Card transactions frequently include location data from the merchant terminal. Wallet transactions frequently omit it. Card transactions carry the merchant's own category code. Wallet transactions may carry the wallet provider's code instead. Card descriptors are inconsistent but information-rich. Wallet descriptors are more consistent but information-poor.

| Aspect | Card transaction | Wallet transaction |

|---|---|---|

| Merchant name | Often explicit and merchant-defined | Often generic or wallet-formatted |

| Location data | Frequently present (city, state) | Frequently missing or stripped |

| Payment method clarity | Clear card usage | Wallet hides underlying card |

| Descriptor format | Merchant-controlled | Wallet-standardized |

| Context signals | Rich and direct | Abstracted or reduced |

These differences are not accidental. They are by design. Wallets prioritize user privacy and payment security, which means minimizing the merchant-specific information that flows through the payment chain. From an enrichment perspective, this means fewer deterministic signals to work with.

What Data Is Lost or Abstracted by Digital Wallets

Understanding exactly which enrichment-relevant signals wallets reduce or remove helps developers anticipate where enrichment quality will be lower and design their products accordingly.

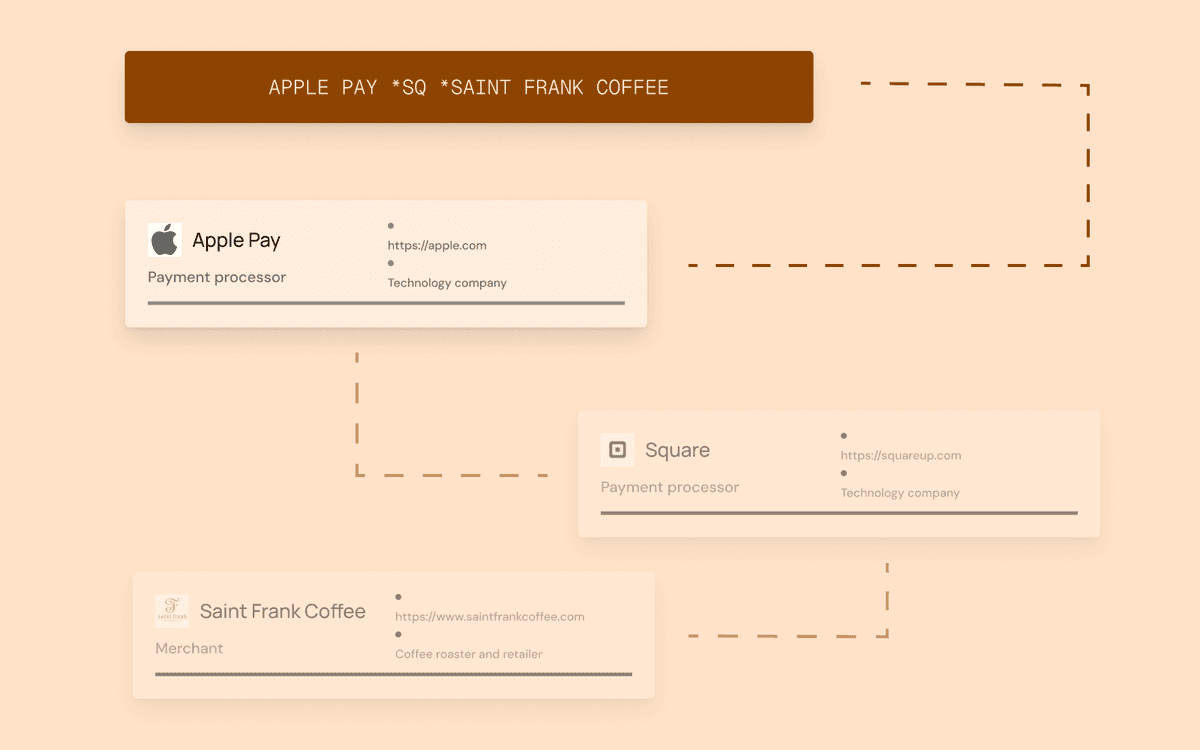

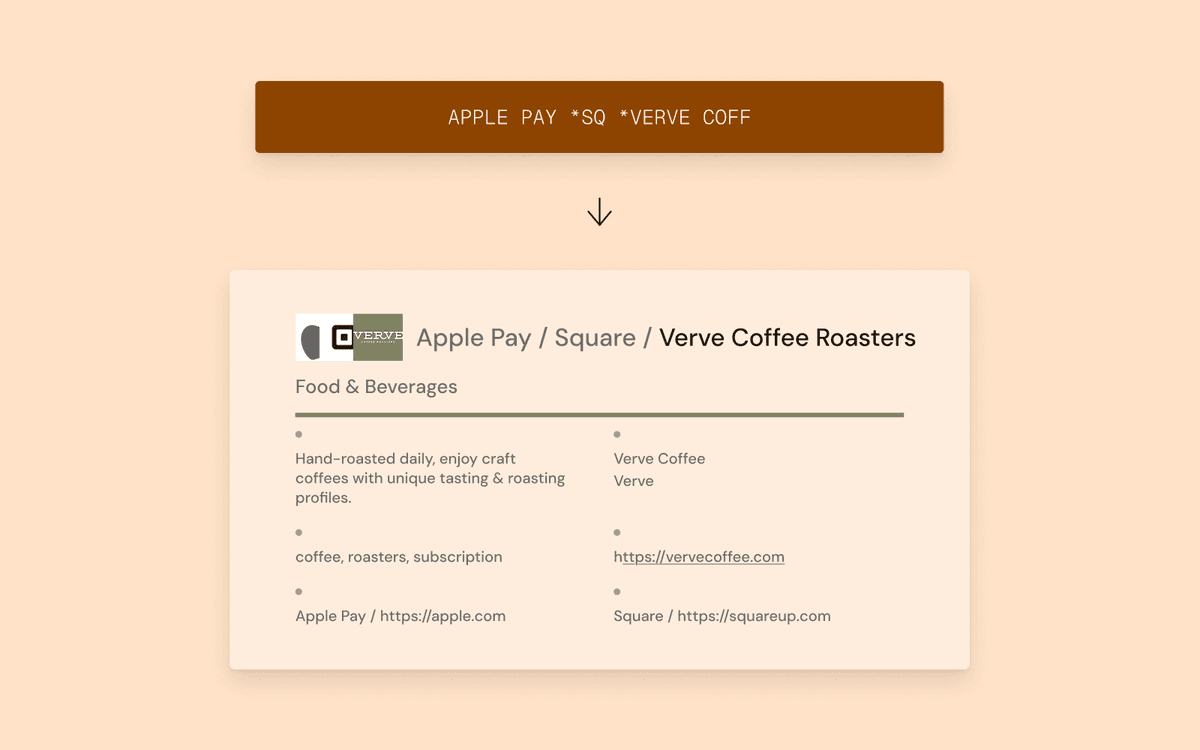

Original merchant descriptors are the most important loss. Where a direct card transaction might show VERVE COFFEE ROASTERS SAN FRANCISCO CA, the same transaction through Apple Pay might appear as APPLE PAY *SQ *VERVE COFFEE or simply APPLE PAY *SQUAREUP. The merchant's own descriptor, which is the primary input for most enrichment systems, is overwritten or compressed by the wallet and any intermediary payment facilitators.

Store identifiers and branch numbers are frequently stripped. Many merchants include store numbers in their descriptors to help with internal reconciliation. Wallets have no reason to preserve this information, so it is often removed. This reduces the ability of enrichment systems to distinguish between different locations of the same chain.

Physical location information is often missing from wallet transactions. In-store card payments typically include at least a city and state. Wallet transactions frequently omit location entirely because the wallet provider does not relay it or the terminal does not transmit it to the wallet in the same way.

Acquirer-specific metadata that enrichment systems use as secondary signals (such as terminal IDs, acquirer references, and processing codes) may be reformatted or dropped by the wallet layer.

Payment processor information becomes ambiguous. A transaction through Apple Pay that was processed by Square for a small coffee shop involves at least three entities (Apple, Square, and the coffee shop), but the transaction descriptor may only clearly identify one or two of them. Separating the wallet from the processor from the merchant requires sophisticated entity resolution.

Why Standard Enrichment Approaches Fail for Wallet Transactions

Enrichment systems that work well for traditional card transactions often underperform significantly on wallet transactions because their primary techniques rely on exactly the signals that wallets abstract.

String matching and merchant lookup, the backbone of most dataset-driven enrichment systems, depends on having a recognizable merchant name in the transaction descriptor. When the descriptor shows the wallet or processor name instead of the merchant name, lookup-based systems either return the wrong entity (identifying "Apple Pay" as the merchant) or return nothing useful at all.

MCC-based categorization is particularly unreliable for wallet transactions. The MCC code attached to a wallet transaction may reflect the wallet provider's business classification, the payment facilitator's classification, or a generic code that tells you nothing about the actual purchase. A coffee purchase through Apple Pay via Square might carry an MCC code for "technology" or "financial services" rather than "eating places."

Fixed merchant datasets that map descriptor patterns to known merchants struggle with wallet transactions because the descriptor patterns are different from what these datasets were built to match. A dataset entry for "STARBUCKS" will match STARBUCKS #12345 SEATTLE but may not match APPLE PAY *STARBUCKS or GOOGLEPAY *STARBUCKS MOBILE ORDER because the wallet prefix changes the pattern.

Location-based enrichment that uses geographic hints in transaction descriptors becomes largely ineffective when wallets strip location information. Without a city, state, or postal code in the descriptor, location enrichment must rely on alternative data sources or contextual inference.

Common Wallet Transaction Edge Cases

Beyond the general challenges, wallet-based payment flows introduce specific edge cases that are uncommon with direct card payments and that trip up enrichment systems not specifically designed for them.

Subscriptions paid through wallets frequently produce changing descriptors. A monthly subscription to Spotify paid directly by card might consistently show SPOTIFY AB every month. The same subscription paid through Apple Pay might alternate between APPLE.COM/BILL, APPLE PAY *SPOTIFY, or ITUNES.COM/BILL depending on how the billing is routed. This makes recurring transaction matching, which relies on identifying identical transactions, unreliable.

Different merchants can produce identical wallet descriptors. When multiple small businesses use the same payment facilitator (like Square or Stripe), their transactions through a wallet may all appear with the facilitator's name and no distinguishing merchant information. Two completely different coffee shops might both show as APPLE PAY *SQ *COFFEE in the bank feed.

Cross-border wallet transactions add currency and regional complexity on top of the existing abstraction. A wallet transaction made while traveling may carry a different currency code, a foreign processor identifier, and a descriptor format that reflects the local payment conventions of the merchant's country rather than the consumer's home country.

In-app purchases routed through platform wallets (Apple's App Store, Google Play) show the platform as the merchant rather than the developer whose app the user actually paid. This means that a game purchase, a productivity tool subscription, and a streaming service subscription can all appear identically as APPLE.COM/BILL, a single descriptor covering thousands of completely different products and categories.

Delayed settlement in some wallet payment flows causes mismatched timestamps between when the user remembers making a purchase and when the transaction appears in their bank feed. This temporal disconnect makes it harder for users to correlate transactions with their own memory and increases the importance of accurate enrichment to compensate.

How Context-Aware Enrichment Solves Wallet Challenges

Because wallets remove direct identifiers, wallet transaction enrichment depends more heavily on contextual signals and intelligent reasoning than traditional descriptor matching. This is where the architecture of the enrichment system matters most.

Advanced enrichment APIs address wallet challenges through several complementary strategies. Intermediary detection and separation is the most critical capability. Rather than treating the entire transaction descriptor as a single entity, sophisticated systems identify each layer of the payment chain separately: the wallet provider, the payment facilitator, and the underlying merchant. Triqai's enrichment engine specifically separates intermediaries from merchants, so a transaction that passes through Apple Pay via Square to a local coffee shop can identify all three entities with their respective logos, names, and metadata.

For example, sending a wallet-obscured transaction to a context-aware enrichment API:

{ "title": "APPLE PAY *SQ *VERVE COFF", "country": "US", "type": "expense"}Returns a response that separates each entity in the payment chain:

{ "merchant": { "name": "Verve Coffee Roasters", "logo": "https://logos.triqai.com/images/verve-coffeecom" }, "intermediary": { "name": "Square", "type": "payment_facilitator" }, "wallet": { "name": "Apple Pay", "type": "wallet" }, "category": { "primary": "Food and Drink", "secondary": "Coffee and Cafes" }, "confidence": 0.88}AI reasoning applied to partial signals allows the system to make intelligent inferences even when the descriptor alone is insufficient. By analyzing the combination of the descriptor fragments, the transaction amount, the currency, the country, the time of day, and patterns from similar transactions across other users, reasoning-based systems can identify the most likely merchant even with limited direct evidence.

Web-derived context provides real-time information that fixed datasets cannot. When a descriptor includes a partial merchant name or a location hint, AI-powered systems can cross-reference this against web data sources (business directories, map services, review platforms, delivery apps) to resolve the merchant identity with higher confidence. This dynamic approach means the system can identify merchants it has never encountered before, rather than being limited to a pre-compiled list.

Historical transaction patterns for the same user provide additional context. If a user regularly makes purchases at a specific coffee shop with a clear card transaction, and a new wallet transaction appears with a similar amount at a similar time from the same geographic area, the system can infer a likely match even when the descriptor is ambiguous.

Confidence scoring becomes especially important for wallet transactions. Because enrichment confidence is structurally lower for wallet payments, the API must provide accurate confidence indicators so downstream applications can make informed decisions about how to present the data.

How Triqai Enriches Wallet Transactions

Triqai is specifically designed to handle the complexity of modern payment flows, including digital wallet transactions. Several capabilities make this possible.

Triqai's intermediary detection system separates payment processors from the underlying merchants across the full payment chain. When a wallet transaction passes through Apple Pay and is processed by Square for a local business, Triqai identifies the wallet (Apple Pay) as the payment method, Square as the intermediary, and the actual business as the merchant. Each entity receives its own name, logo, website, and confidence score. This level of detail is not available from enrichment systems that treat the entire descriptor as a single entity.

Triqai's AI-powered merchant resolution uses real-time web context to identify merchants even when the transaction descriptor is minimal or wallet-formatted. Rather than relying on a fixed merchant dataset, the system reasons about what the transaction most likely represents based on all available signals, including information gathered from maps, business directories, and digital footprints. This means Triqai can identify millions of merchants and entities dynamically, including small or regional businesses that no static dataset would ever cover.

For location enrichment of wallet transactions, Triqai uses web-derived context and AI reasoning to provide store-level location data across 150+ countries, even when the transaction descriptor omits geographic information. By cross-referencing the identified merchant against web sources rather than depending solely on descriptor-embedded location strings, Triqai resolves locations that fixed-dataset systems miss entirely.

The result is that wallet transactions enriched through Triqai receive significantly more accurate and detailed enrichment than what descriptor-matching or dataset-driven systems can achieve. Because Triqai considers more context and reasons through each transaction before returning a result, it avoids false matches while the confidence scores honestly reflect the remaining uncertainty inherent in wallet payment data.

Best Practices for Handling Wallet Transactions in Your Product

Developers building financial products should expect wallet transactions to behave differently from card transactions and design their applications accordingly.

Use confidence scores to adapt your UI presentation. Here is a practical pattern for wallet-aware display logic:

function formatWalletTransaction(enrichment, rawDescription) { const { merchant, wallet, confidence } = enrichment; const walletLabel = wallet ? `via ${wallet.name}` : ""; if (confidence >= 0.8) { return { name: merchant.name, subtitle: walletLabel, logo: merchant.logo }; } if (confidence >= 0.5) { return { name: `${merchant.name} (?)`, subtitle: walletLabel, logo: wallet?.logo }; } return { name: rawDescription, subtitle: walletLabel, logo: wallet?.logo };}When enrichment confidence is high, display the enriched merchant name, logo, and category with full confidence. When confidence is moderate, consider showing the enriched name alongside the original descriptor so users can verify. When confidence is low, fall back to showing the wallet name and the raw descriptor rather than risking a wrong merchant identification.

Design your transaction feed to clearly indicate the payment method. Users understand that they paid "via Apple Pay" and this context helps them recall the transaction even when the merchant information is limited. Showing the wallet or platform logo alongside any available merchant information provides visual clarity.

Do not treat wallet transactions as lower-quality data in your analytics. Wallet payment volume is growing rapidly. In some demographics and markets, wallet transactions already outnumber direct card payments. Digital wallets now account for 53% of global e-commerce transactions, exceeding card payments in the online channel, according to Worldpay's Global Payments Report 2024. If your spending analytics, budgeting tools, or financial insights ignore or downgrade wallet transactions, you will miss an increasingly large portion of your users' financial activity.

Plan for improving enrichment over time. As enrichment APIs process more wallet transactions and learn from user corrections, accuracy improves. Design your data architecture to support re-enrichment of historical wallet transactions when better models become available.

Test your enrichment pipeline specifically against wallet transaction patterns. Include Apple Pay, Google Pay, Samsung Pay, and PayPal transactions in your validation dataset, and track accuracy metrics separately for wallet versus non-wallet transactions. This helps you identify wallet-specific quality gaps and prioritize improvements.

The Future of Wallet Transaction Enrichment

Wallet transaction volume has grown tenfold over the past decade and continues to outpace all other payment types, driven by consumer demand for convenience and security. As wallet adoption increases, the percentage of transactions that are structurally harder to enrich will continue to grow. Enrichment systems that rely primarily on descriptor matching and static databases will see their overall accuracy decline as wallet transactions become a larger share of the transaction mix.

The future belongs to context-aware, AI-powered enrichment systems that can reason about transactions rather than simply looking them up in a fixed dataset. These systems treat the wallet abstraction layer not as an obstacle but as one signal among many, combining it with web context, user patterns, and transaction metadata to produce accurate enrichment regardless of the payment method.

For fintech developers, the practical implication is straightforward: choose a transaction enrichment API that is specifically designed to handle wallet payments, not one that treats them as an afterthought. Test your provider against your actual wallet transaction data, and design your product to gracefully handle the structural uncertainty that wallet payments introduce.

Conclusion

Digital wallets have modernized payments for consumers, but they have introduced genuine complexity for any system that needs to understand what those payments represent. Wallet transaction enrichment is harder because wallets intentionally abstract, tokenize, and standardize payment information, reducing the merchant-specific signals that enrichment depends on.

The solution is not to wait for wallets to expose more data (they will not, because privacy is their value proposition) or to accept degraded enrichment quality. The solution is to use enrichment systems that go beyond descriptor matching and fixed datasets, applying AI reasoning, web-derived context, intermediary separation, and confidence scoring to produce accurate results even when the input data is deliberately sparse.

Triqai's transaction enrichment API is built for this reality. By using web data and AI to reason through each transaction rather than forcing a match against a static merchant list, Triqai separates wallets from processors from merchants, reasons about partial signals, and provides transparent confidence scores so your product can handle every transaction with appropriate confidence. For a broader view of transaction enrichment fundamentals, read our complete guide to transaction enrichment.

Frequently asked questions

Tags

Related articles

Written by

Wes Dieleman

Founder & CEO at Triqai

December 23, 2025

Wes founded Triqai to make transaction enrichment accessible to every developer and fintech team. With a background in software engineering and financial data systems, he leads Triqai's product vision, AI enrichment research, and API architecture. He writes about transaction data, merchant identification, and building developer-first fintech infrastructure.